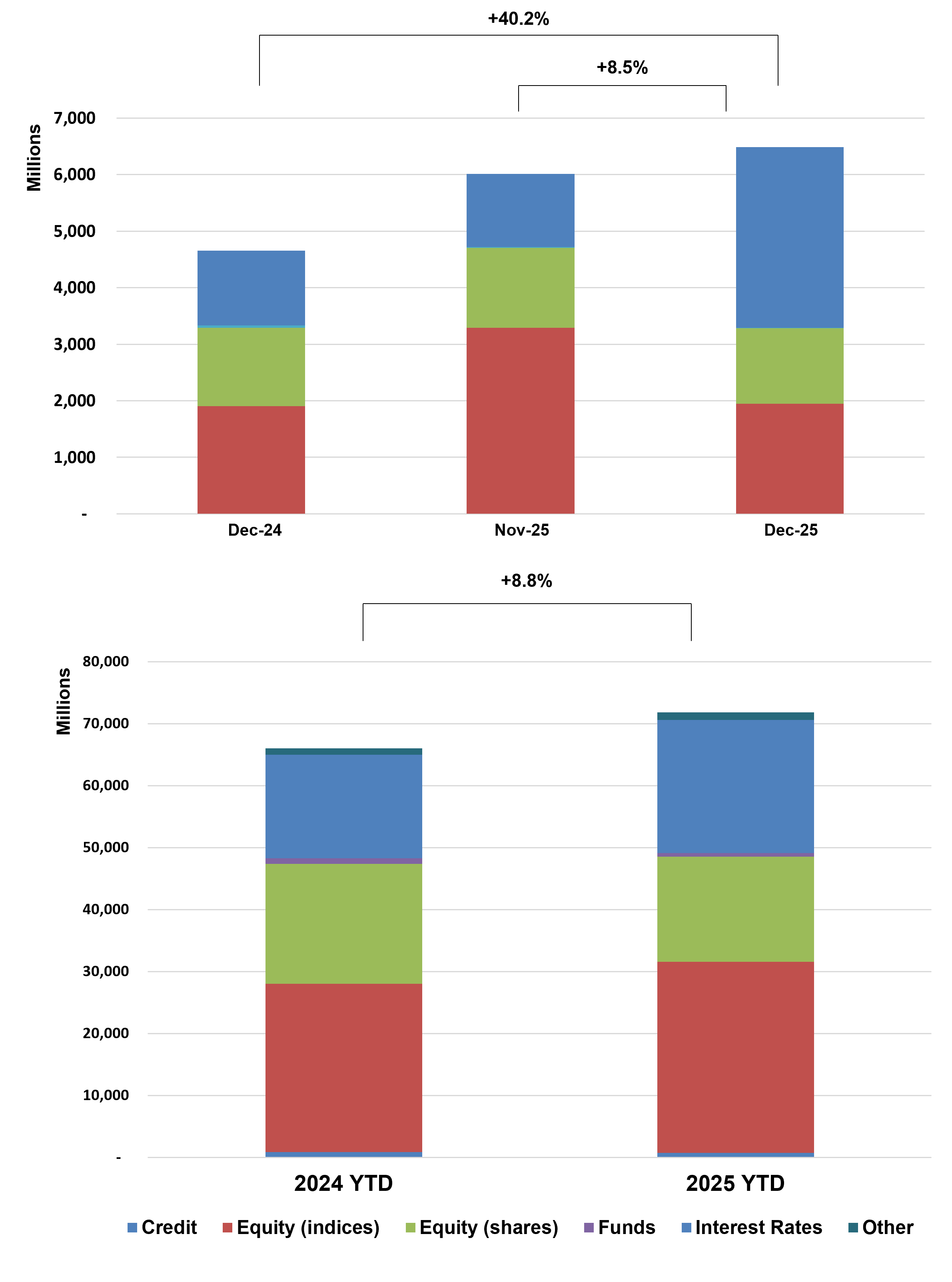

As expected, FY25 issuance reached €71.8bn, representing +8.8% YoY growth, comfortably exceeding the €70bn threshold.

• December sales reached €6.6 billion, representing a 40.2% year-on-year increase.

• Product mix remained well balanced. Growth products retained leadership with a 39.7% market share, followed by Income products at 32.8%, which continued to gain relative traction through the year. Capital-protected structures accounted for 27.4% of issuance, stabilising after weaker mid-year dynamics.

Methodology & Notes

This report is based on SPi’s proprietary database of structured products distributed in France. Figures reflect best-effort estimates based on available market data at the time of publication.

Disclaimers

Data Disclaimer (Best Effort / Completeness)

The information presented in this report is based on data collected from a variety of public and proprietary sources. While reasonable care has been taken to ensure accuracy, the data may be incomplete, subject to revisions, or may not capture the entirety of the market. SPi makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information.

General Disclaimer

This document is provided for informational purposes only and does not constitute investment advice, an offer, or a recommendation to buy or sell any financial instrument or to adopt any investment strategy. The views expressed are those of SPi at the date of publication and are subject to change without notice. Past performance is not indicative of future results.

SPi accepts no liability for any loss arising from the use of this report or its contents.