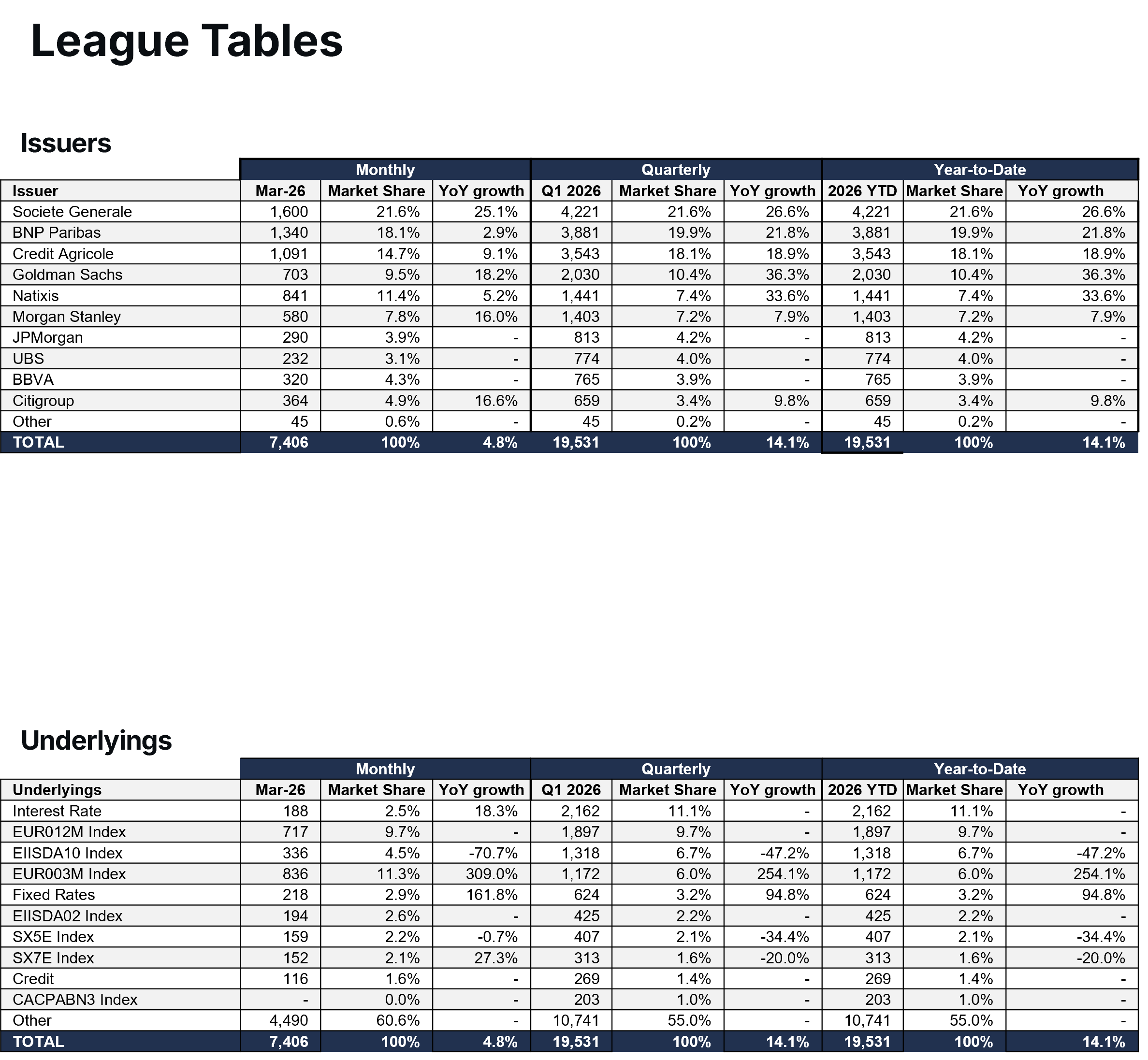

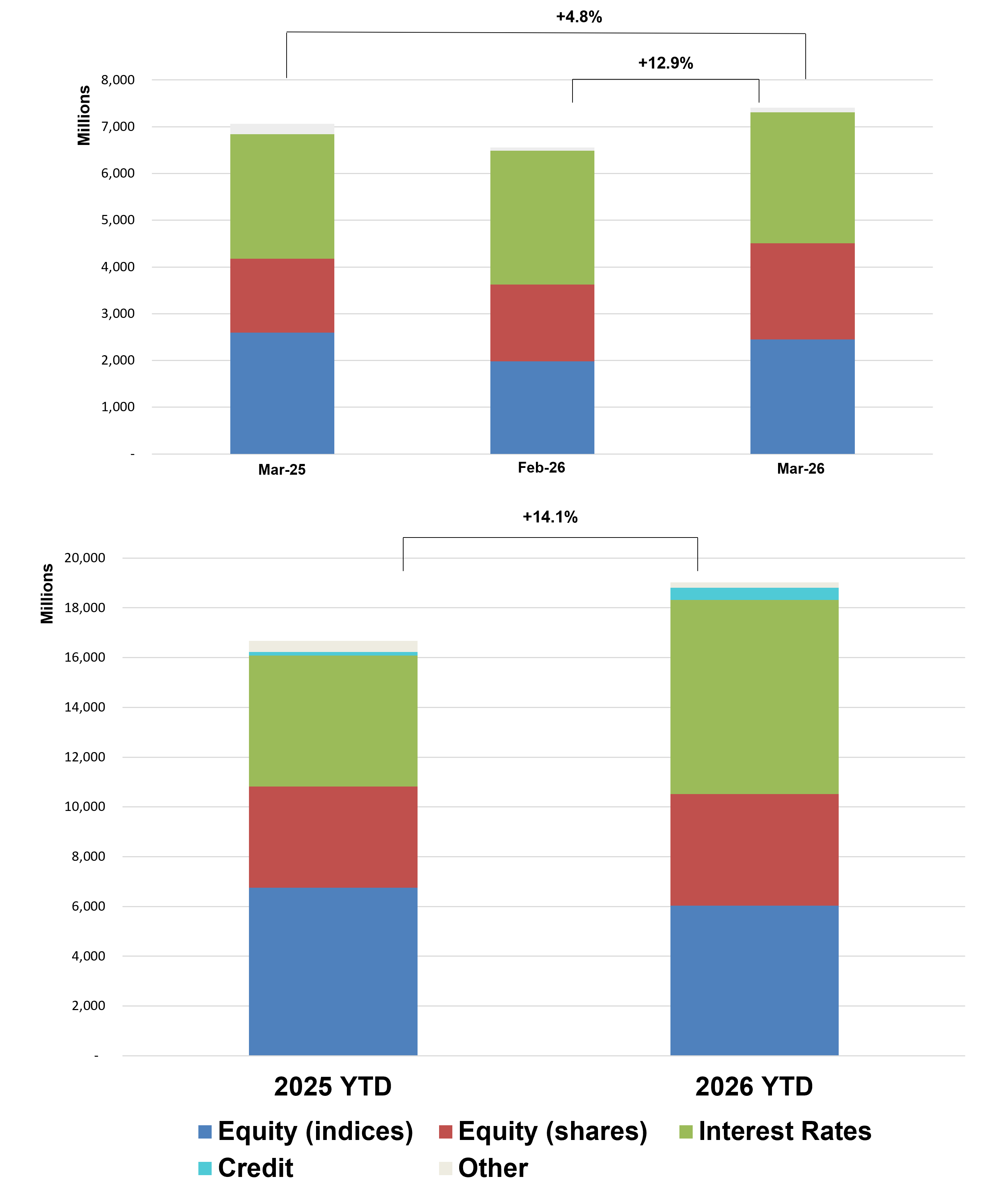

French structured products issuance reached €7.4bn in March, bringing 2026 YTD volumes to €19.5bn, a strong 14.1% increase YoY.

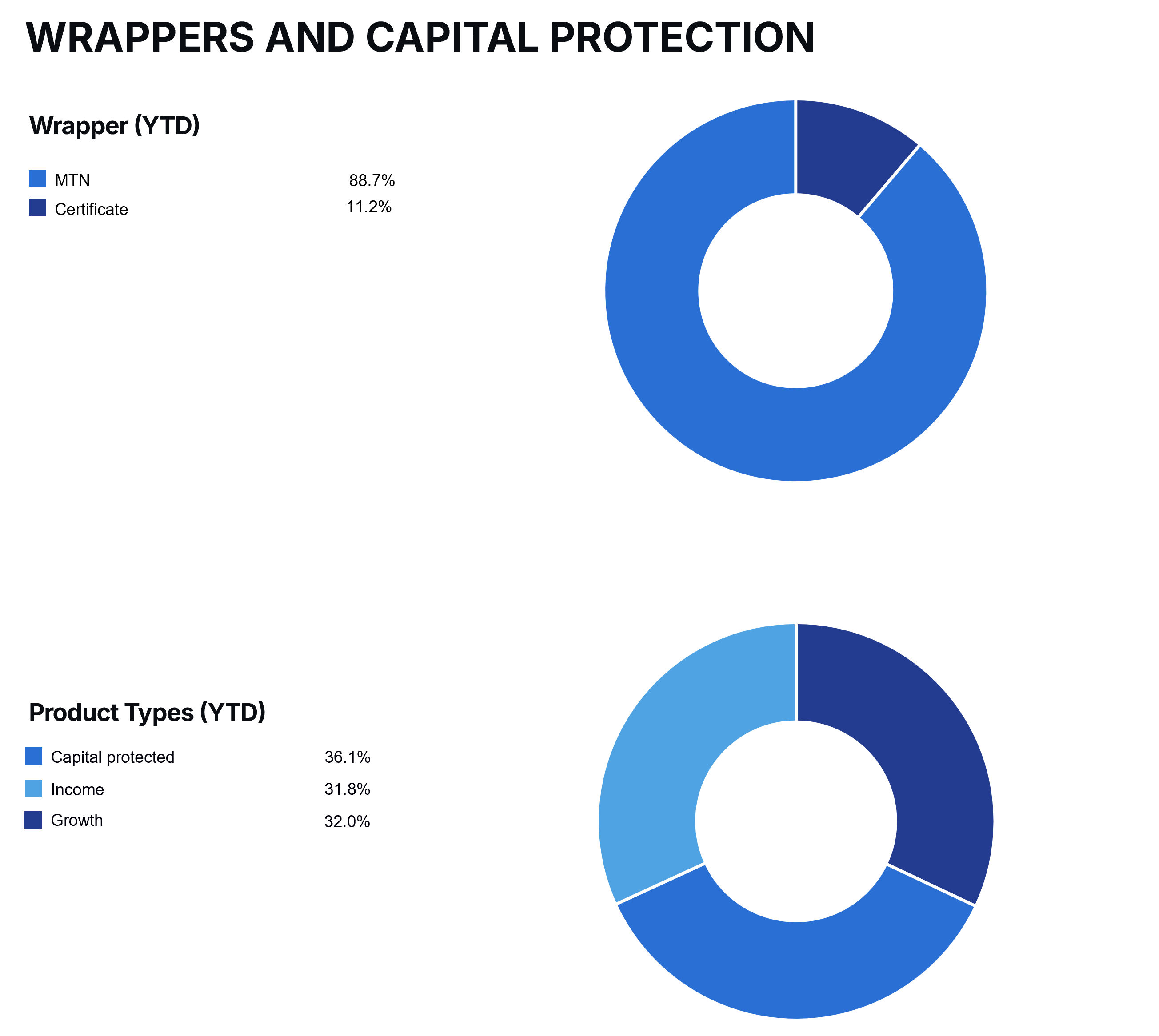

• Product mix remains broadly balanced in 2026 YTD, with a slight tilt toward capital preservation. Capital Protected products lead issuance with a 36.1% market share, followed by Growth products at 32.0%, while Income products account for 31.9%. Compared to the prior year, the mix appears more evenly distributed, suggesting investors continue to seek participation strategies while maintaining downside protection in an uncertain macro environment.

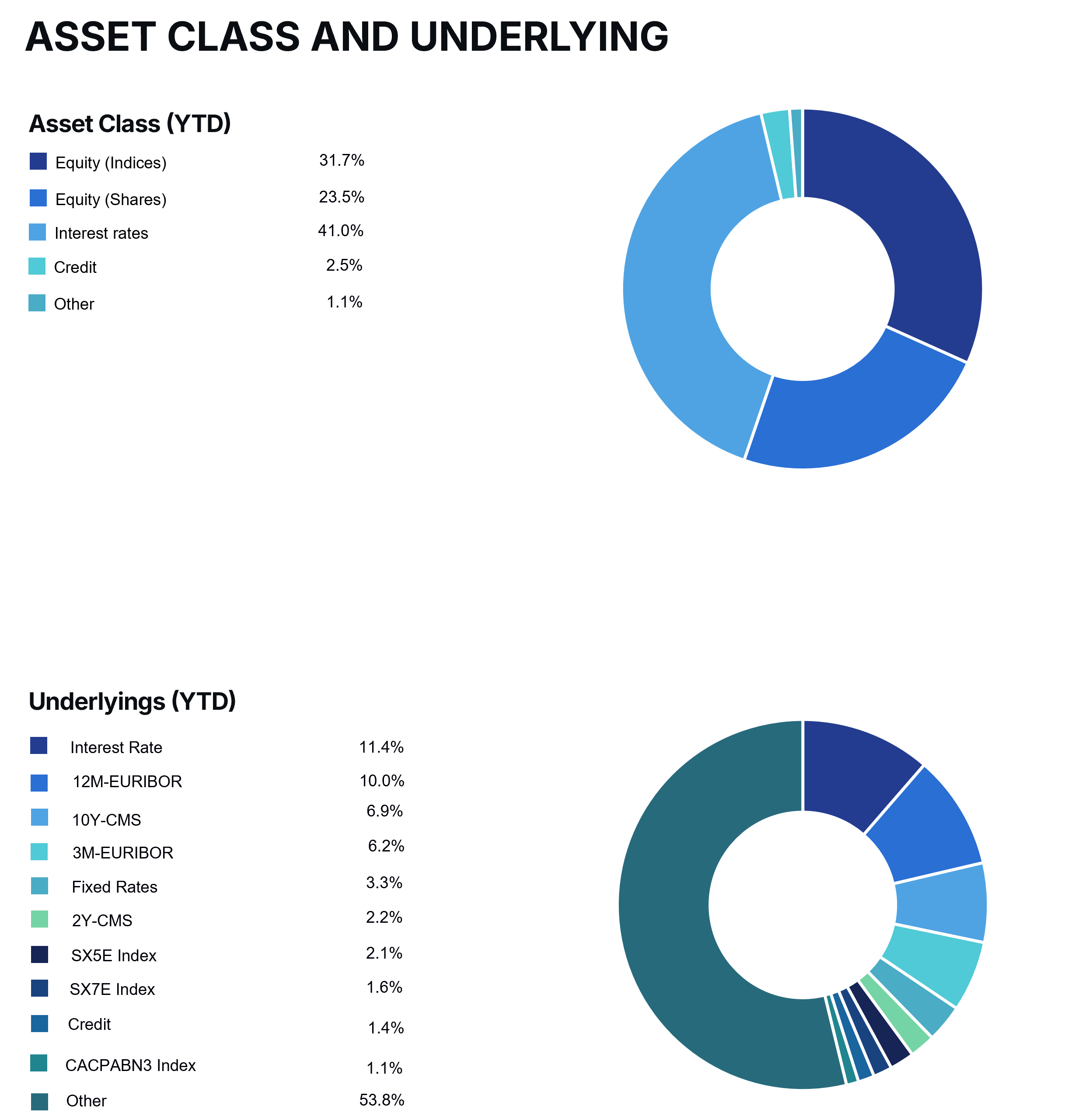

• Investor appetite has shifted decisively toward Interest Rates, now the dominant asset class at 41.0% of total issuance, up materially from 31.6% in 2025 YTD. This reflects sustained demand for rates-linked structures amid persistent uncertainty around monetary policy and yield levels. Equity index-linked products remain significant at 31.7%, though down from 40.5% last year, indicating a moderation in broad market beta exposure. Meanwhile, Equity share-linked issuance increased to 23.5%, versus 24.4% in 2025 YTD, remaining broadly stable and signalling continued selective interest in idiosyncratic equity opportunities. Credit-linked issuance rose meaningfully to 2.6%.

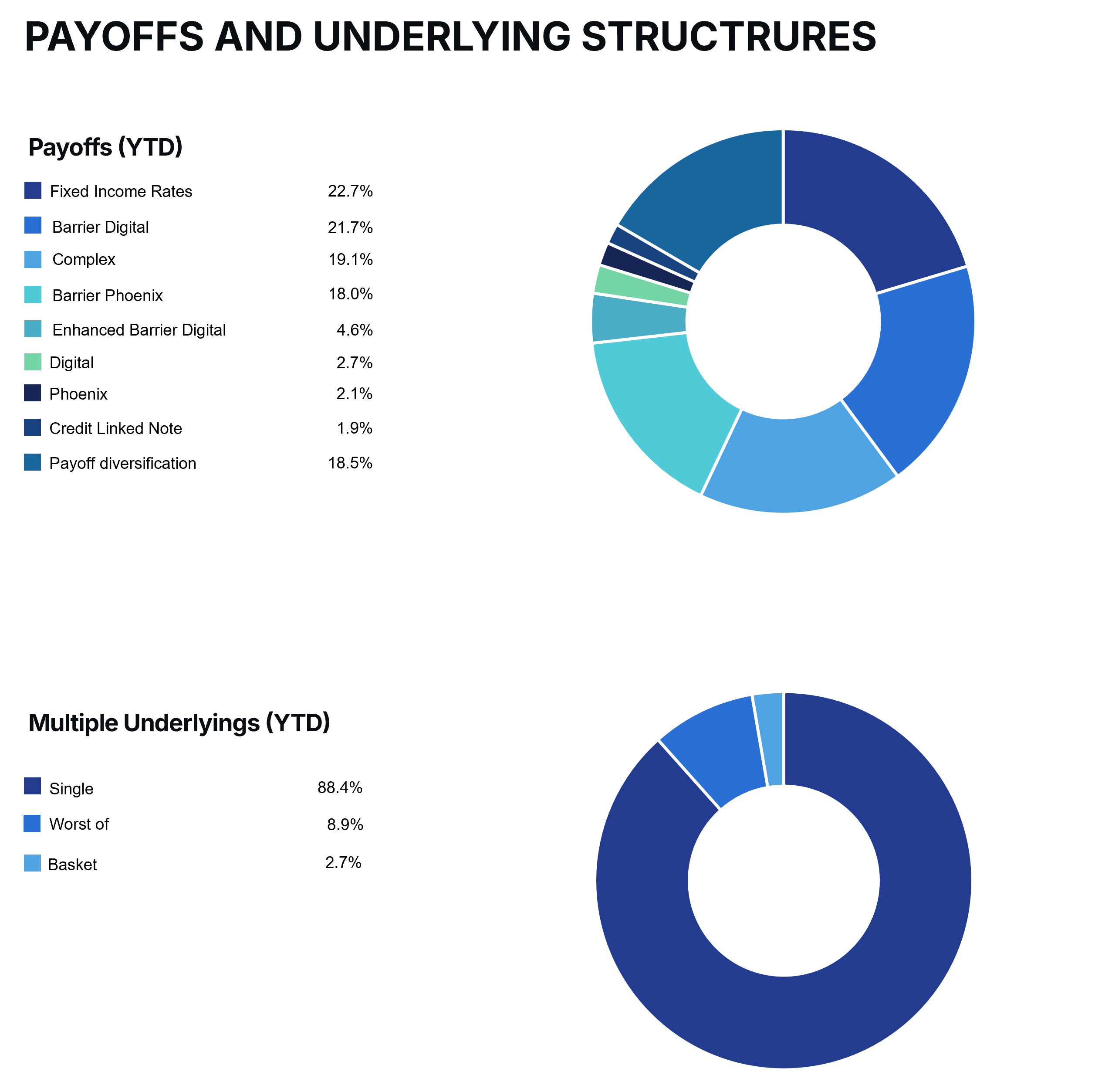

• Single-underlying products continue to dominate issuance, representing 88.4% of total volumes. At the same time, worst-of structures increased slightly to 8.9%, highlighting continued investor demand for yield-enhancing, correlation-sensitive payoffs. Basket structures remain marginal at 2.7%, continuing their structural decline as simpler and more transparent structures remain preferred.

• In terms of payoff typology, Fixed Income / Rates-linked payoffs are now the largest segment, accounting for 22.7% of issuance, overtaking Barrier Digital structures at 21.7%. Complex structures represent 19.1%, underscoring sustained demand for more tailored or bespoke solutions, while Barrier Phoenix products account for 18.0%. Together, these four payoff categories represent over 80% of total issuance, indicating continued concentration in structured yield and rates-driven solutions. Meanwhile, enhanced barrier digital structures account for 4.6%, with traditional digital (2.7%) and phoenix (2.2%) products remaining niche. Credit Linked Notes represent 1.9%, while the remaining 18.5% reflects broader payoff diversification.

• Overall, the 2026 YTD profile points to a notable rotation toward interest rate-linked structures and capital-protected solutions, while maintaining significant demand for structured yield formats such as barrier digital and phoenix payoffs. The decline in broad equity index-linked issuance, alongside resilient single-stock and more complex structures, suggests a more selective and defensive investor stance compared to 2025 YTD.

MARKET SNAPSHOT

• Société Générale leads the French structured products market in 2026 YTD, with €4.2bn of issuance, corresponding to a 22.2% market share. Volumes increased by a strong 26.6% YoY, supported by robust and consistent activity throughout Q1, including €1.6bn issued in March alone (+25.1% YoY). The bank has strengthened its leadership position versus the start of the year.

• Crédit Agricole ranks second with €3.9bn of issuance and a 20.4% market share. While YTD growth remains modest at +2.4% YoY, the bank posted stronger momentum during the quarter, with Q1 volumes reaching €3.5bn, up 18.9% YoY, suggesting improving recent activity.

• BNP Paribas follows closely with €3.5bn of issuance and an 18.6% market share, up 21.8% YoY. Issuance remained resilient in March at €1.3bn (+2.9% YoY), maintaining its position among the top three market leaders.

• Goldman Sachs continues to stand out as one of the fastest-growing major issuers, with €1.4bn of issuance and a 7.6% market share. Volumes increased by 33.6% YoY, while Q1 issuance rose 36.3% YoY to €2.0bn, confirming a continued expansion in market presence and distribution.

• Natixis recorded €1.4bn of issuance (7.4% market share), though volumes declined 22.9% YoY despite a strong Q1 performance (+33.6% YoY), indicating weaker recent issuance dynamics.

• Morgan Stanley posted €0.9bn of issuance (4.8% market share), down 33.0% YoY, reflecting softer issuance despite a still positive Q1 trend (+7.9% YoY).

• JPMorgan Chase (4.3% market share), UBS (4.1%), and BBVA (4.0%) continue to build presence from a lower base. Meanwhile, Citigroup saw issuance decline to €0.7bn (3.5% share), down 34.7% YoY, despite a stronger March (+16.6% YoY).

• Overall, the issuer landscape in 2026 YTD remains concentrated among leading French domestic players, with Société Générale, Crédit Agricole, and BNP Paribas together accounting for over 61% of total issuance. International issuers such as Goldman Sachs continue to gain market share, while dispersion in quarterly versus YTD growth trends suggests shifting issuance momentum across the competitive landscape.