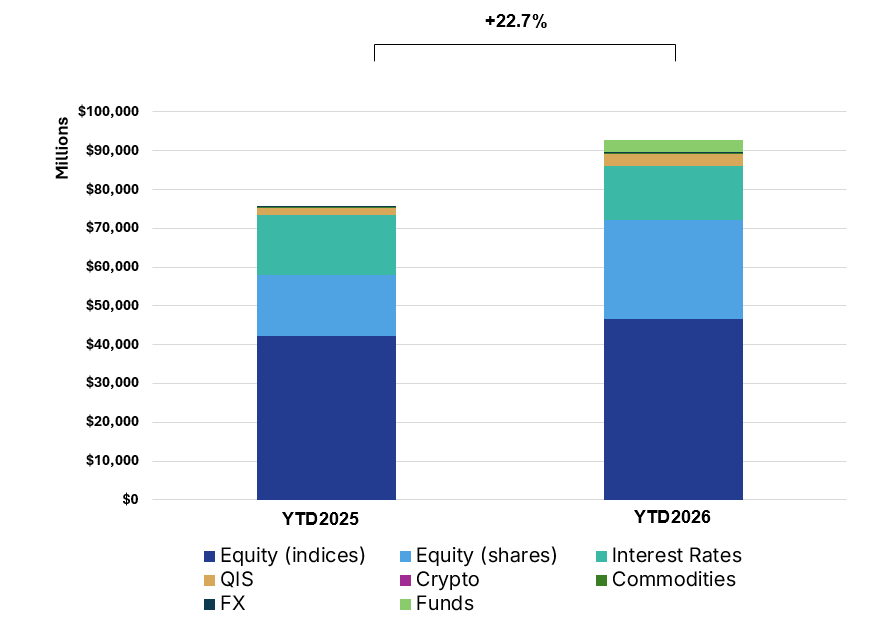

U.S. Structured Products Issuance Reaches USD 92.9Bn YTD (+22.7% YoY) as Growth and Income Strategies Dominate.

Key Highlights

• Product Mix: Growth and Income strategies dominate, accounting for approximately 80% of issuance, while Capital Protected products represent nearly 20% of volumes.

• Structure Mix: Single-underlying products lead at 58.9%, while Worst-of structures account for 36.3%, reflecting sustained demand for enhanced yield and autocallable-style payoffs.

• Payoff Structures: Barrier Phoenix products lead at 31.9%, followed by fixed income/rates-linked structures at 13.4%, with participation and digital variants remaining meaningful contributors.

• Underlying Trends: Equity-linked issuance remains concentrated in major U.S. benchmarks, led by SPX Index at 12.4%, alongside multi-index exposures incorporating NDX, RTY, and INDU.

Market Overview

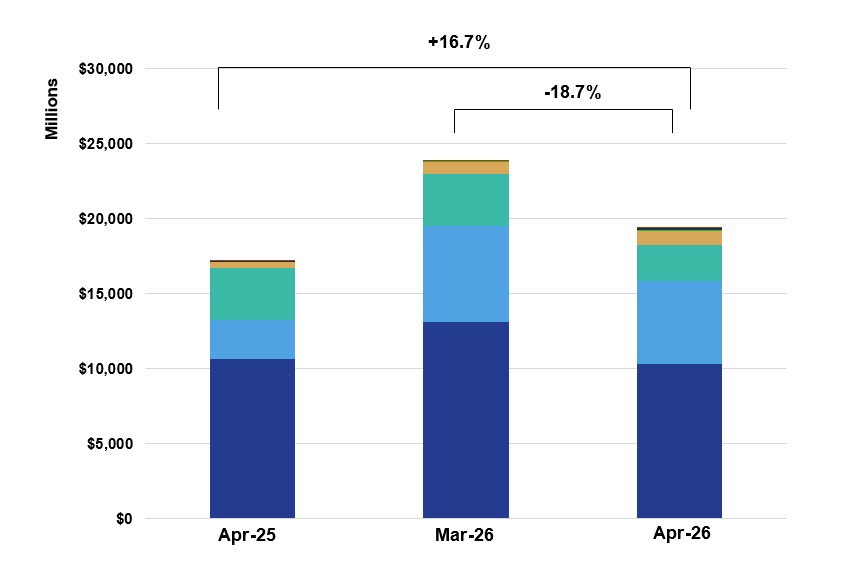

April 2026 confirms continued strength in the U.S. structured products market, with year-to-date issuance reaching USD 92.9Bn (+22.7% YoY). Momentum remained strong across both quarterly and monthly activity, with QTD volumes up 24.4% YoY and monthly issuance increasing 16.7% YoY. Growth and Income strategies continue to dominate issuance, together accounting for approximately 80% of total flow, while Capital Protected solutions represent nearly 20%.

Structurally, the market remains led by Single Underlying products, which account for 58.9% of issuance, while Worst-of structures represent 36.3%, reinforcing continued investor demand for enhanced yield and autocallable-style formats. Payoff construction remains anchored by Barrier Phoenix products, which represent 31.9% of total issuance, followed by fixed income/rates-linked structures at 13.4%. Participation and digital variants also continued to contribute meaningful share across the structured solutions landscape.

Underlying exposure remains concentrated in major U.S. equity benchmarks, led by SPX Index at 12.4%, alongside multi-index combinations incorporating NDX, RTY, and INDU exposures. Broader diversification across additional underlyings represented 62.7% of total issuance, highlighting the continued breadth of market activity beyond the most widely used benchmark exposures.

By asset class, Equity-linked issuance remains the dominant driver, with Index-linked Equity products totaling approximately USD 46.5Bn and Equity Share-linked issuance reaching USD 25.7Bn. Interest Rate-linked issuance totaled USD 13.8Bn, while QIS, FX, Crypto, Credit, Commodities, and ETF-linked structures remained comparatively smaller but continued to support broader diversification across product offerings. Overall, April reflects a strong U.S. market characterized by sustained growth, continued dominance of Growth and Income strategies, and persistent demand for equity-linked and barrier-based structures.

Methodology & Notes

This report is based on SPi’s proprietary database of structured products distributed in the United States. Figures reflect best-effort estimates based on available market data at the time of publication.

Disclaimers

Data Disclaimer (Best Effort / Completeness)

The information presented in this report is based on data collected from a variety of public and proprietary sources. While reasonable care has been taken to ensure accuracy, the data may be incomplete, subject to revisions, or may not capture the entirety of the market. SPi makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information.

General Disclaimer

This document is provided for informational purposes only and does not constitute investment advice, an offer, or a recommendation to buy or sell any financial instrument or to adopt any investment strategy. The views expressed are those of SPi at the date of publication and are subject to change without notice. Past performance is not indicative of future results.

SPi accepts no liability for any loss arising from the use of this report or its contents.