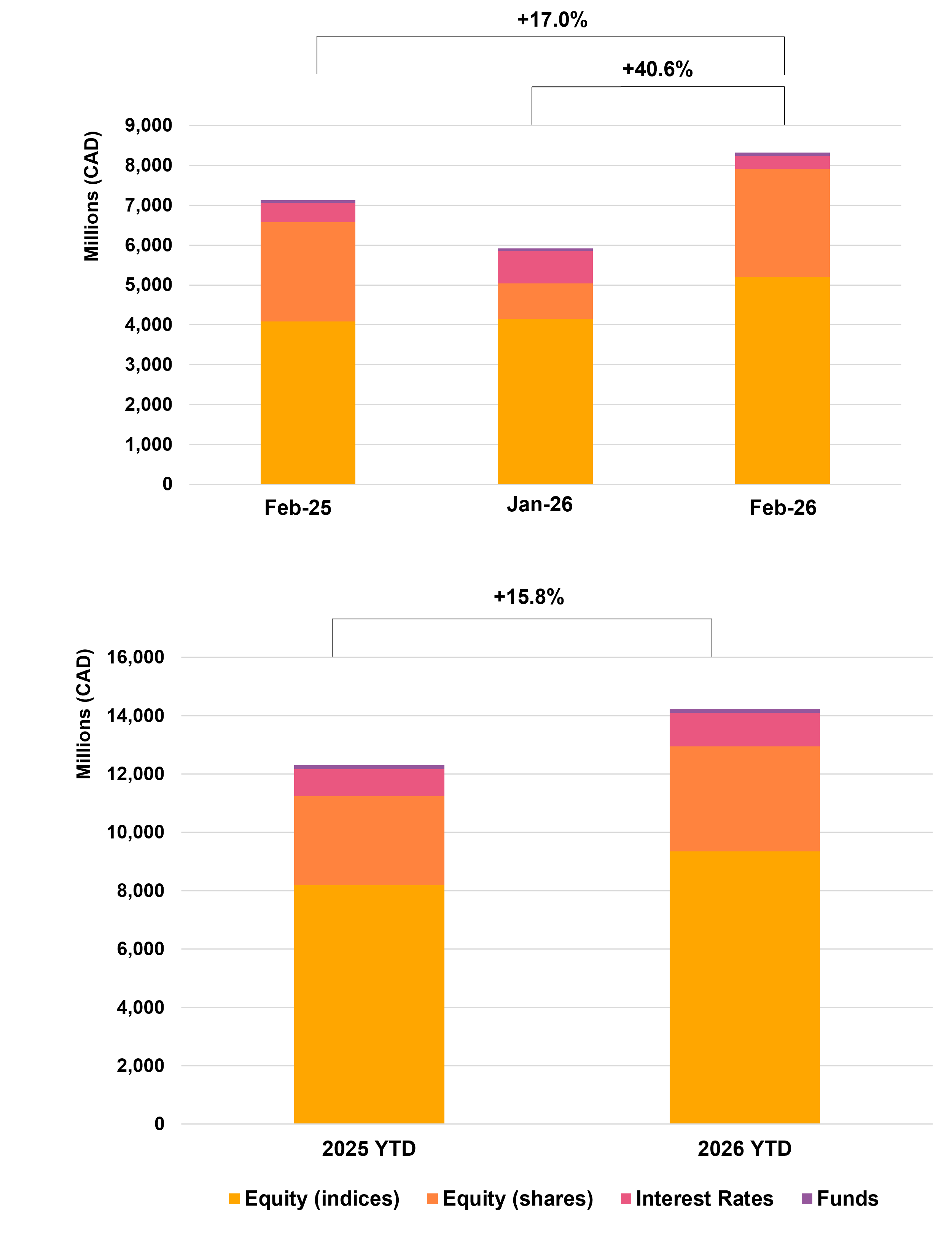

Canadian Structured Products Issuance Reaches CAD 8.3Bn (+17.0% YoY) as Income and Growth Drive YTD Expansion

Key Highlights

• Product Mix: Income (42.0%) and Growth (~21.2%) gain traction, while Capital Protected (~36.8%) declines, confirming a shift toward yield and market-linked exposure.

• Structure Mix: Single-underlying products dominate at ~79.3%, while baskets (~20.5%) decline, reinforcing preference for simplified structures.

• Payoff Structures: Barrier Phoenix (~39.2%) leads, followed by Barrier Digital Plus (~18.5%) and Capped Protected Participation (~21.8%), highlighting dominance of income-oriented and participation structures.

• Underlying Trends: Proprietary indices dominate, with leading underlyings below 10% share, reflecting diversified index usage and customization.

Market Overview

February 2026 confirms the continued strength of the Canadian structured products market, with issuance reaching CAD 8.3Bn (+17.0% YoY) and year-to-date volumes at CAD 14.2Bn (+15.8% YoY). Growth is increasingly driven by a rotation toward income and growth strategies, as income products expand strongly and growth structures accelerate, while capital-protected products decline, reflecting a clear shift in investor preference toward higher-yielding, market-linked solutions. Structurally, the market remains heavily concentrated in single-underlying formats (~79%), with basket structures losing ground, in contrast to trends observed in the U.S. Payoff construction continues to be anchored by Barrier Phoenix (~39%) and Barrier Digital Plus (~18%), reinforcing the dominance of conditional income strategies, while the decline in capped protected participation highlights reduced demand for fully protected formats. On the underlying side, the continued dominance of proprietary indices—with leading indices such as SOLCD265 (~8%)—confirms the structural shift toward customized benchmarks designed for yield enhancement, while traditional indices like the S&P 500 lose share. Overall, February reflects a strong, yield-driven market, characterized by rising risk appetite, increasing product complexity, and sustained innovation in index design and payoff structures.

Methodology & Notes

This report is based on SPi’s proprietary database of structured products distributed in Canada. Figures reflect best-effort estimates based on available market data at the time of publication.

Disclaimers

Data Disclaimer (Best Effort / Completeness)

The information presented in this report is based on data collected from a variety of public and proprietary sources. While reasonable care has been taken to ensure accuracy, the data may be incomplete, subject to revisions, or may not capture the entirety of the market. SPi makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information.

General Disclaimer

This document is provided for informational purposes only and does not constitute investment advice, an offer, or a recommendation to buy or sell any financial instrument or to adopt any investment strategy. The views expressed are those of SPi at the date of publication and are subject to change without notice. Past performance is not indicative of future results.

SPi accepts no liability for any loss arising from the use of this report or its contents.