Canada Structured Products Issuance Reaches CAD 82.5Bn (+26.1% YoY) as December Closes at Record CAD 8.2Bn

Key Highlights

• Product Split: Notes CAD 52.4Bn (+35.4% YoY) vs. GICs CAD 30.0Bn (+13.1% YoY), confirming stronger growth in market-linked structures.

• Monthly Dynamics: December notes issuance reached a record CAD 5.70Bn, driven by PAR Notes (CAD 4.86Bn) and PPNs (CAD 0.84Bn); GICs declined to CAD 2.5Bn (-13.0% YoY).

• Product Mix: Capital-protected products lead (46.4%), followed by Income (35.9%) and Growth (17.7%), highlighting a protection-heavy market.

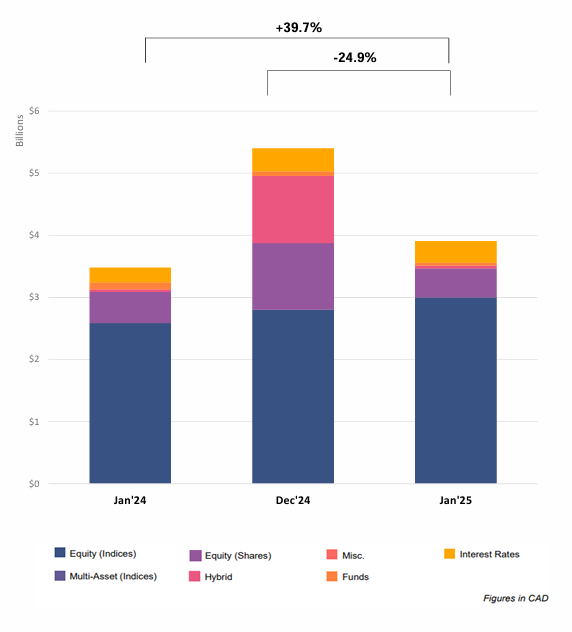

• Underlying & Structure: Single underlyings dominate (74.5%) vs. baskets (25.1%); equity indices lead (67.0%), followed by single stocks (25.7%).

• Payoff Preferences: Barrier phoenix (>33% share) remains dominant; followed by Capped Protected Participation (29.9%) and Barrier Digital Plus (15.1%).

• Thematic Indices: SOLCD265 Index gained traction (CAD 694M in December), while SOLBEW27 and SOLCLDAR declined; SOLBEW30 (CAD 401M) and SOCAEN75 (CAD 346M) also notable.

• Performance: Realized returns on matured products increased, peaking at 11.0% in December, reflecting strong equity market carry-through.

Market Overview

The Canadian structured products market delivered a standout performance in 2025, with issuance reaching CAD 82.5Bn (+26.1% YoY) and exceeding expectations, culminating in a record December (CAD 8.2Bn). Growth was primarily driven by strong expansion in Notes (+35.4% YoY), significantly outpacing GIC growth (+13.1%), highlighting a structural shift toward market-linked solutions. The market remains distinctly protection-oriented, with capital-protected products accounting for 46.4% of issuance, while still maintaining meaningful allocations to income and growth strategies. Structurally, single-underlying products dominate (74.5%), reflecting simpler product design preferences. The continued dominance of equity indices (67%) underscores the central role of equity markets in driving issuance, while barrier phoenix structures (>33%) confirm strong demand for yield-enhancing solutions. The rise of proprietary indices such as SOLCD265 further highlights ongoing innovation in underlying design, while elevated realized returns (11%) reinforce positive investor outcomes. Overall, Canada exhibits a robust, protection-heavy market profile, combining strong issuance growth, record monthly activity, and stable structural preferences.

Methodology & Notes

This report is based on SPi’s proprietary database of structured products distributed in Canada. Figures reflect best-effort estimates based on available market data at the time of publication.

Disclaimers

Data Disclaimer (Best Effort / Completeness)

The information presented in this report is based on data collected from a variety of public and proprietary sources. While reasonable care has been taken to ensure accuracy, the data may be incomplete, subject to revisions, or may not capture the entirety of the market. SPi makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information.

General Disclaimer

This document is provided for informational purposes only and does not constitute investment advice, an offer, or a recommendation to buy or sell any financial instrument or to adopt any investment strategy. The views expressed are those of SPi at the date of publication and are subject to change without notice. Past performance is not indicative of future results.

SPi accepts no liability for any loss arising from the use of this report or its contents.