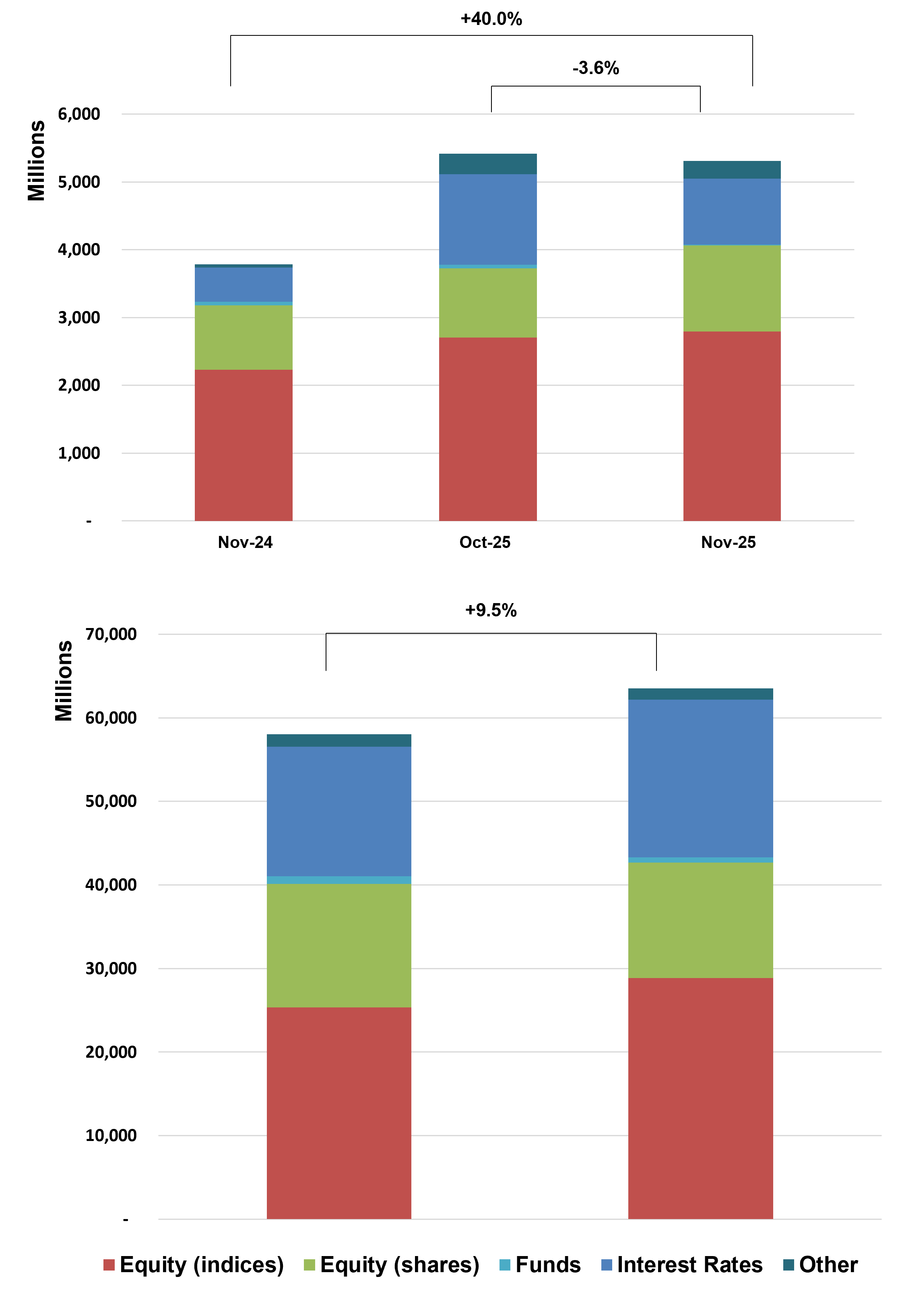

France Structured Products Issuance Reaches EUR 63.6Bn (+9.5% YoY) as November Volumes Jump to EUR 5.4Bn (+40.0% YoY)

Key Highlights

• Issuance Dynamics: Year-to-date volumes reached EUR 63.6Bn (+9.5% YoY); November issuance totalled EUR 5.4Bn (+40.0% YoY).

• FY Outlook: At the current pace, FY25 issuance is expected to exceed EUR 70Bn (~+13% YoY).

• Product Mix: Growth leads at 38.4%, closely followed by Income (37.6%), with Capital Protected declining to 23.9%, its lowest level since August.

• Underlying Trends: Equity indices reached EUR 28.8Bn (+13.9% YoY); rates EUR 18.9Bn (+21.6% YoY); single stocks EUR 13.8Bn (-6.7% YoY).

• Structure Mix: Single-underlying products dominate at 87.7%, vs. worst-of (9.0%) and baskets (3.3%).

• Decrement Trends: Decrement index issuance reached EUR 17.0Bn (+25.5% YoY), driven by Decrement Points (+43.2%), offset by a decline in Percentage Decrements (-42.8%).

• Barrier Structures: Knock-in barrier products remained stable in count (-0.5% YoY) while volumes increased +9.1% YoY.

Market Overview

November data reflects a strong rebound in French structured product issuance, with monthly volumes rising to EUR 5.4Bn (+40.0% YoY), bringing year-to-date issuance to EUR 63.6Bn (+9.5% YoY). The market remains on track to exceed EUR 70Bn in 2025, confirming a solid growth trajectory despite earlier softness. A key development is the tight convergence between growth and income products, with growth (38.4%) only marginally ahead of income (37.6%), reflecting increasing investor demand for yield-oriented solutions. Meanwhile, capital-protected products (23.9%) have declined to their lowest share in recent months, signaling a shift toward higher-return structures. The market continues to show a dual allocation between equity indices and rates, with both asset classes delivering solid growth, while single-stock exposure declines further, indicating preference for diversified underlyings. Structurally, the dominance of single-underlying products (87.7%) remains intact. The continued expansion of decrement index issuance (+25.5% YoY) and stable volumes in knock-in barrier products highlight ongoing innovation in structured payoff design. Overall, November reflects a resilient and evolving market, with strong issuance momentum, shifting product mix toward income, and sustained demand for engineered yield solutions.

Methodology & Notes

This report is based on SPi’s proprietary database of structured products distributed in France. Figures reflect best-effort estimates based on available market data at the time of publication.

Disclaimers

Data Disclaimer (Best Effort / Completeness)

The information presented in this report is based on data collected from a variety of public and proprietary sources. While reasonable care has been taken to ensure accuracy, the data may be incomplete, subject to revisions, or may not capture the entirety of the market. SPi makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information.

General Disclaimer

This document is provided for informational purposes only and does not constitute investment advice, an offer, or a recommendation to buy or sell any financial instrument or to adopt any investment strategy. The views expressed are those of SPi at the date of publication and are subject to change without notice. Past performance is not indicative of future results.

SPi accepts no liability for any loss arising from the use of this report or its contents.